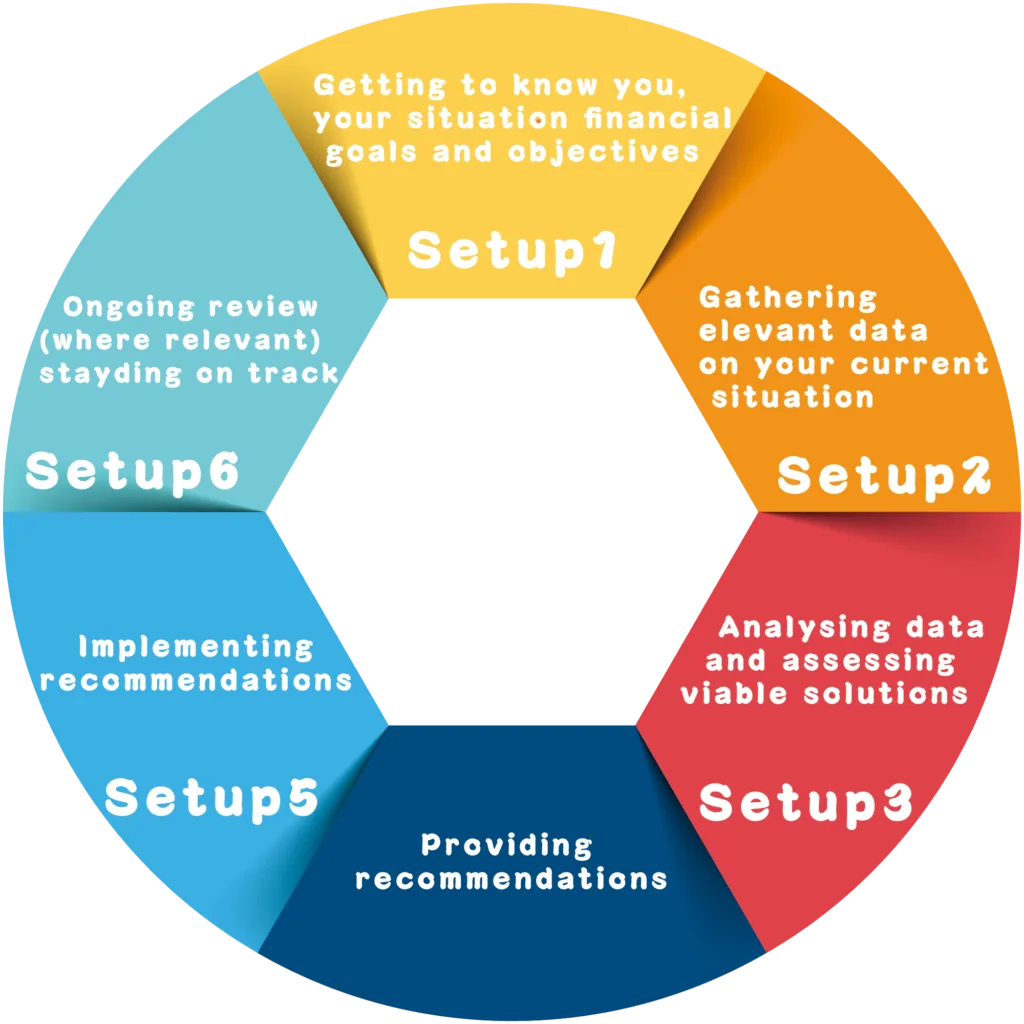

mortgage services, guiding you to a secure future and

protecting what matters most, every step of the way.

bespoke life, health, asset, and business insurance

solutions to expertly safeguard what matters most.

solutions, securing your dream home or investment

with tailored guidance and expert service.

“The loan process with bsi brokers was incredibly easy and straightforward. The team helped me every step of the way, providing clear guidance and answering all of my questions. The approval was quick, and I received the funds much faster than expected. I highly recommend their loan services for anyone who needs financial assistance!”

“I was impressed with how bsi brokers handled my loan application. Their team was responsive, knowledgeable, and really took the time to ensure I understood all my options. The loan was approved in no time, and the terms were exactly what I needed. If you're looking for a hassle-free loan experience, they’re the ones to go to.”

“BSI Brokers made applying for a loan so simple. I had been struggling with other options, but their team helped me secure a loan that fit my financial needs. The process was fast, and I appreciated how transparent they were throughout. I would absolutely use them again in the future for any financial needs..”

"The loan process with bsi brokers was very smooth and stress-free. The staff guided me through every step and explained everything clearly. I was able to get the loan I needed without any hidden fees or surprises. The entire experience was positive, and I highly recommend them to anyone in need of a reliable loan service."

"BSI Brokers helped me secure a loan with the best interest rate I could find. They took the time to understand my needs and tailored a solution that worked for me. The application process was smooth, and I had access to my funds quickly. I'm so grateful for their help and will definitely consider them for any future financial needs."

"The loan service provided by bsi brokers was exceptional. They were professional, quick to respond, and helped me get approved for a loan with great terms. I felt confident throughout the process, and their team was always available to answer my questions. I would highly recommend them to anyone looking for a reliable and efficient loan provider."